In Guernsey, the terms "insurance broker" and "insurance intermediary" are often used interchangeably, but they have distinct roles and definitions under the GFSC regulations.

An insurance broker acts as an intermediary between clients and insurance companies. Their primary role is to represent the client, providing advice on insurance needs and helping to find the best insurance policies available in the market. Brokers typically work with multiple insurers to offer a range of options to their clients. They are responsible for:

- Advising clients on their insurance requirements.

- Arranging insurance contracts between clients and insurers.

- Assisting with claims and policy adjustments.

While all insurance brokers are intermediaries, not all intermediaries are brokers. Intermediaries can also include agents who may represent a single insurer, unlike brokers who typically offer products from multiple insurers.

Applications

Any person wishing to act as an Insurance Intermediary or a Captive Manager must submit an application to the GFSC and be licensed under section 4 of the Law. The various contents of each licensee’s application are detailed in the applicable Insurance Rules and Guidance.

Both licensees must meet Minimum Capital Requirements (MCR) of the higher of £25,000 and 125% of their Professional Indemnity Insurance deductible or excess with specific criteria on what are considered to be approved assets.

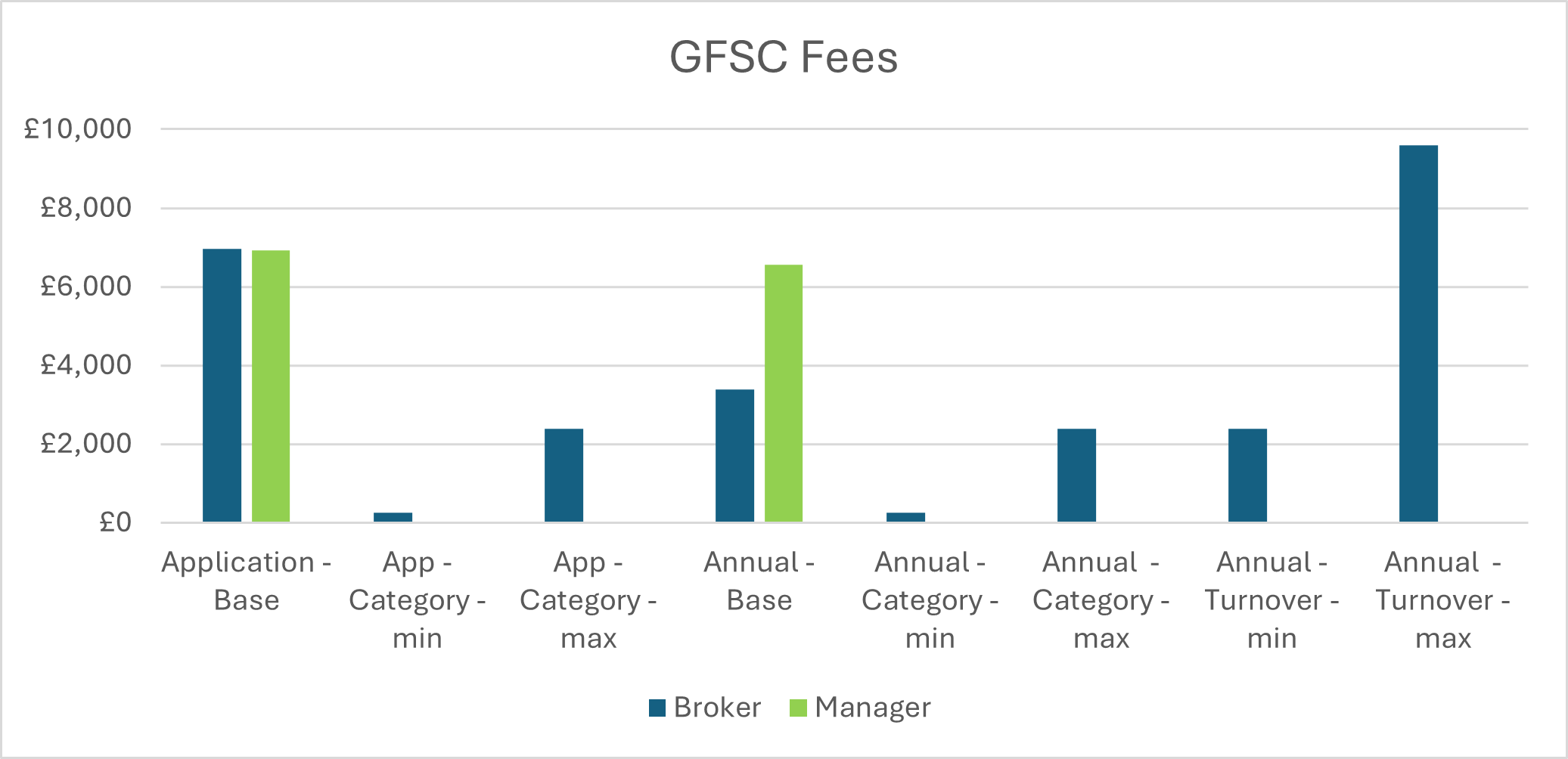

Fees

The regulatory fees payable to the GFSC are quite different between the 2 categories and much higher for Intermediaries.

The Application Fee for Captive Managers is £6,920 and for Intermediaries, it is £6,965. However, if the intermediary wants to add additional categories to their license, there are extra costs:

- For general personal lines - £245.

- For general commercial lines and long-term life insurance - £485.

- For long-term regular premium insurance - £735.

- For long-term single premium insurance (insurance element) - £2,390.

Annual fees are due by 31 January each year for licences in effect on 1 January of that year.

The Annual Fee for Captive Managers is £6,565 and they must demonstrate to the GFSC that each insurer for which they act underwrites only the risks of the insurer's parent or its associated party. Otherwise, the fee is £10,995.

For Intermediaries, it is £3,380 with additional costs for extra categories which are the same cost as the application fees and fees based on Turnover received from customers in the Bailiwick of Guernsey which range from £2,390 to £9,590.

Both have identical inaccurate and late filing and payment penalties.

Compliance

Intermediaries must comply with detailed annual returns and public disclosure obligations, ensuring transparency and accountability. In comparison Captive Managers have more simplified and specific regulatory standards tailored to captive insurance management and how they conduct business thus in comparison have a lower compliance cost and administrative burden.

While both categories must comply with the GFSC AML Handbook, only Captive Managers and Insurance Intermediaries carrying on long term business must report to the GFSC using the Financial Crime Risk Return. This distinction ensures that Intermediaries involved in long-term business, which typically carries higher financial crime risks due to the nature of the products, are subject to more stringent reporting requirements.

The ongoing supervision by the GFSC of each type of licensee and notification requirements are generally the same.

Risk Management

Intermediaries are required to implement comprehensive risk management practices, including conflicts of interest policy, management of client monies and dealing with customer complaints.

Captive Managers focus more on their core business activities and the related party that is insured, with less stringent risk management practices compared to Intermediaries. They will also have a higher level of oversight from the insurer’s stakeholders as to how service is provided to the captive.

Representatives

In accordance with section 15 of the Law, every Insurance Intermediary is required to authorise one or more Authorised Insurance Representative (“AIR”) to act on its behalf in order to advise clients on their insurance requirements and arrange contracts of insurance.

In November 2021, the GFSC issued the Code of Conduct for Authorised Insurance Representatives (“the Code”) which specifies the 10 Principles of Conduct of Finance Business in fulfilling the AIRs’ duties.

The Insurance Intermediary is required to monitor and supervise its AIRs to a high degree as it retains full responsibility for the actions and conduct of these individuals. The Insurance Intermediary is also required to ensure that its AIRs are, and continue to be, fit and proper as defined in Schedule 4 of the Minimum Criteria for Licensing (“MCL”) in the Law. It is mandatory for all AIRs who advise on long term insurance business to attain the relevant minimum insurance qualifications.

AIRs who advise on any insurance policy or product considered to be long term business falling under Schedule 1 of the Law, with certain exceptions, must be appointed as Financial Advisers and attain a minimum qualification as required by the GFSC.

The GFSC has published a guidance note on training and competency schemes and details of the qualifications which are available from its website.

Captive Managers are responsible for managing the day-to-day operations of the licensed insurers under their management which are established and owned by companies to insure their own risks. As such the stakeholder is the company that is insuring its own risks.

The services provided include the provision of underwriting, accounting and claims management as well as providing assistance with other key areas such as compliance and corporate governance. One of the most important functions performed by a Captive Manager is for an individual to act as General Representative to the licensed insurers under their management and like AIRs must adhere to the MCL in the Law. It should also be noted that if the Captive Manager were ever to deal with the general public, then it must also appoint an Authorised Insurance Representative and fulfil the requirements noted above.

The duties of the General Representative are detailed in Part 5 of The Insurance Business Rules and Guidance, 2021.

Insurance Rules & Guidance

Intermediaries and Captive Managers have their own set of Insurance Rules and Guidance which provide standards to be met and guidance on how to comply with the Law and its regulatory framework. Although there are similarities, some of the key differences are noted below:

| Insurance Intermediaries Rules & Guidance 2021 | The Insurance Managers Rules & Guidance 2021 |

| Client Advice | Y | N |

| Annual Returns | Y - detailed

| Y - Limited |

| Public Disclosure of Information | Y | N |

| Authorised Insurance Representative (AIR) | Y | N - Unless AIR appointed |

| Categorise Clients | Y | N |

| Compliance Arrangements | Y | N |

| Training Competency | Y | N |

| Outsourcing | N- except compliance | Y |

| Disclosure to Clients/ Transparency | Y | N |

| Complaints Handling Process | Y | Limited |

| Client Monies | Y | N - unless requested to hold client monies |

| Client Facing Reporting | Y | N |

| Conflicts of Interest | Y - detailed | N - Limited |

| Gap Analysis | N | Y |

Conclusion

BDO's expertise in regulatory compliance can help Insurance Intermediaries and Captive Managers navigate the complex requirements set by the GFSC. By conducting thorough reviews of the insurance regulations, we can ensure that your company is adhering to the necessary standards and guidelines and provide comprehensive internal audit services to evaluate and improve the policies, procedures, and controls that are in place. This includes assessing risk management practices, compliance arrangements and the effectiveness of internal controls, thereby enhancing overall operational efficiency and regulatory compliance.

Please send your enquiry to advisory@bdo.gg or email your usual contact at BDO Guernsey.